[ad_1]

(Bloomberg) — Another tech plunge, another shot in the arm for stock quants mounting a big comeback in Wall Street’s awful year.

Most Read from Bloomberg

As the Federal Reserve ramped up its hawkish policy guidance this week on still-raging inflation, the once-booming Faang megapcaps lost a further $568 billion in market value, bringing the cohort’s total capitalization to the lowest since mid-2020.

With rising interest rates spurring an abrupt end to the leadership of Big Tech, the largest technology companies are wielding less and less power over broader indexes, as former high-fliers like Meta Platforms Inc. and Amazon.com Inc. crash anew in the latest wave of selling. Reversing the extremes of the cheap-money years, the capitalization-weighted S&P 500 hit the lowest versus an equal-weighted version of the benchmark since 2019.

All this is a boon for so-called factor investors, who dissect equities according to their math-derived traits, from how cheap equities look to how fast they’ve risen. These funds are typically underweight the tech megacaps and have a propensity to spread out their exposures, a favorable setup in this era of improved market breadth.

In 11 of the last 13 sessions where the S&P 500 has dropped more than 2%, strategies beloved by factor funds like value, quality, momentum and low volatility have all made money, according to Dow Jones’ market-neutral indexes.

“You got a much more diverse opportunity set that allows for more factors to come into play,” said Sean Phayre, head of quantitative investments at Abrdn Investment Management. “Previously 2019, 2020 was a very one-dimensional market.”

Systematic managers who deploy factor strategies in one form or another are on a winning streak. The AQR Equity Market Neutral Fund has rallied anew since October to notch a 21% gain so far this year. The Jupiter Merian Global Equity Absolute Return Fund, which bled assets throughout the tech bull run, is up nearly 7%.

The math whizzes of Wall Street crunch data to find patterns across the entire stock market. That means they’re mostly spreading out their wagers across a vast number of securities. So when market gains are concentrated in a few megacaps, quants almost by definition will own far less of those shares than a cheap-and-cheerful S&P 500 tracker. That was the case in the low-rate years when the Faang block — — Facebook Inc., now known as Meta, Apple Inc., Amazon, Netflix Inc. and Google parent Alphabet Inc. — drove the bull market.

Now a broader group of winners is giving money managers more opportunities. In a reversal of pre-2021 trends, the S&P 500 pulled off an around-8% surge in October even with half of the Faangs falling.

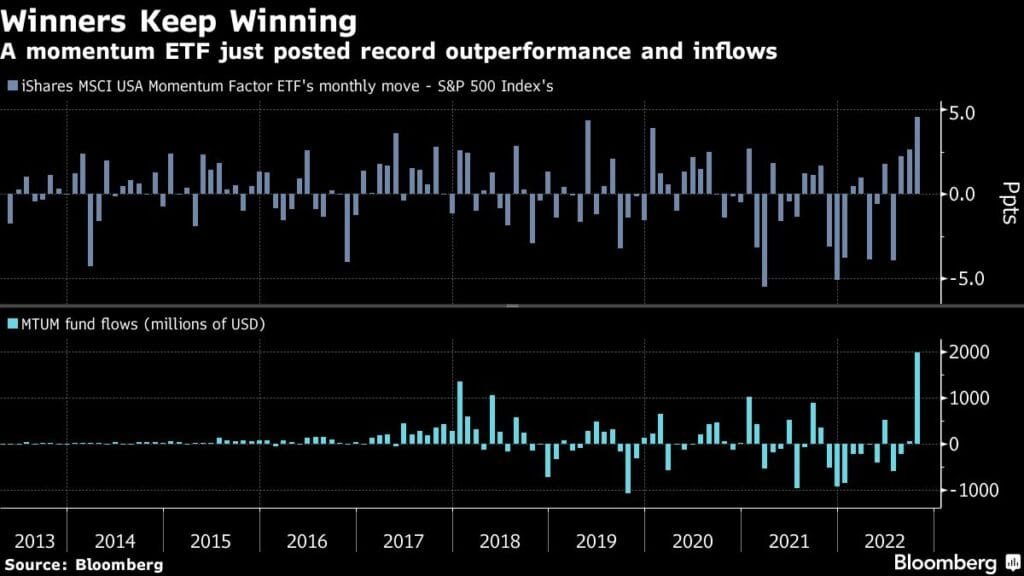

Lately, the momentum factor, a popular quant trade, has also joined the party. A chameleon investing style that simply bets on the past year’s winners, it doesn’t do well at turning points like the start of 2022. But having rebalanced into outperformers like health-care and energy stocks, the strategy has rallied this quarter in a sign of persistent trends driven by sticky inflation.

The $12 billion iShares MSCI USA Momentum Factor ETF (ticker MTUM) drew a record $2 billion in inflows last month after its 13% surge beat the wider market by the most in its nine-year history. A market-neutral version compiled by Bloomberg is on track for the best year since 2015.

“Momentum is the all-weather strategy,” Christopher Harvey, head of equity strategy at Wells Fargo, wrote in a note. He expects more market damage caused by inflation and jobs data, touting momentum strategies as “they have a tendency to perform well” in stressed conditions.

Meanwhile, 87% of high-momentum firms have beaten earnings expectations this season, compared to 70% of the S&P 500, per Harvey. These winning names are also getting rewarded more for good results and punished less for bad ones.

The value strategy of buying cheap shares has also seen another bump with rising rates driving investors away from stocks with high multiples. Meanwhile the low-volatility trade is shining as steadier stocks like health-care names win out.

These trends have only intensified lately with American heavyweights like Amazon, Alphabet and Microsoft posting disappointing earnings — a big turnaround compared to the unbridled tech optimism of the low-rate era.

“The single dimension that was driving those names to excess returns — that model is somewhat broken,” said Phayre at Abrdn. “Come 2021, 2022 there’s a realization there’s going to be some form of payback for all the cheap money.”

–With assistance from Lu Wang.

Most Read from Bloomberg Businessweek

©2022 Bloomberg L.P.

[ad_2]

Source link